One number has been circulating since late 2025 — usually drawn as a tangle of arrows. Nvidia, OpenAI, Oracle, Microsoft, CoreWeave, AMD, Amazon, all wired into each other. Critics call it an ouroboros, the snake eating its own tail. Supporters call it a flywheel. The difference between those two words is the whole story.

The image that keeps going viral is not a chart in the usual sense. It is a circle. Money leaves one company, passes through three others, and arrives back where it started — and at every stop along the way, it is counted as something: an investment, a sale, a backlog, a funding round.

The question worth asking is not whether this looks strange. It does. The question is whether a circle of money is, by itself, a problem. The honest answer is: not necessarily. It depends entirely on one condition — and most of the coverage skips straight past it.

The loop, drawn plainly

Strip away the diagrams and the arrangement is easy to follow.

Nvidia committed to invest up to one hundred billion dollars in OpenAI. OpenAI uses that capital to build data centres. Those data centres are filled with Nvidia chips. So Nvidia’s investment returns to Nvidia as revenue.

Microsoft owns roughly a quarter of OpenAI and is its main cloud provider — meaning OpenAI’s spending becomes Microsoft’s cloud income, some of which buys more Nvidia hardware. OpenAI took a stake in AMD while AMD took orders from OpenAI. Nvidia holds a slice of the cloud builder CoreWeave and committed billions to buy CoreWeave’s spare capacity — capacity stocked, again, with Nvidia chips. Amazon is a major backer of Anthropic, which in turn commits to Amazon’s cloud.

Read it twice and the pattern is unmistakable. The same handful of names keep appearing on both sides of the table: the investor is also the supplier, the customer is also the shareholder.

Why a circle is not automatically a fraud

Here is the part that gets lost in the outrage.

A vendor financing its own customer is one of the oldest arrangements in capitalism. Railroads did it. Telecom equipment makers did it. Aircraft manufacturers still do it today. When an industry needs enormous upfront capital before any revenue arrives, the supplier often lends the buyer the means to buy. That is not a trick. It is how capital-intensive markets get built.

One asset manager described the current wave not as a trap but as a virtuous circle — a way of lining up suppliers, builders and customers fast enough to meet genuinely exploding demand for computing power. On that reading, the loop is simply the visible plumbing of a real boom.

So the arrows alone prove nothing. A circle of money can be a flywheel that bootstraps a genuine market, or a closed loop that manufactures the appearance of one. Both look identical on a diagram. What separates them is not the shape. It is the source of the demand.

The one condition that decides everything

The test is brutally simple, and it is the only test that matters:

Is real money entering the circle from outside it?

If end users — businesses, developers, ordinary customers with no stake in any of these companies — are paying real money for the output, then the loop is a flywheel. The internal financing merely front-loads capacity that genuine demand will fill. The circle is plumbing.

If, instead, the revenue at each stop is mostly the same capital going round again — booked as a sale here, a backlog there, a markup somewhere else — then the circle is closed. It generates the signature of demand without the substance. Each pass inflates everyone’s numbers at once, and the headline figures stop meaning what they appear to mean. As one observer put it: the same hundred billion dollars can show up as a chipmaker’s revenue, a lab’s funding, and a cloud’s backlog — counted three times, earned once.

That is the danger in a single sentence. Not that money moves in a circle, but that a circle can let one dollar be reported as three.

The numbers that keep the debate alive

This is where the figures stop being abstract.

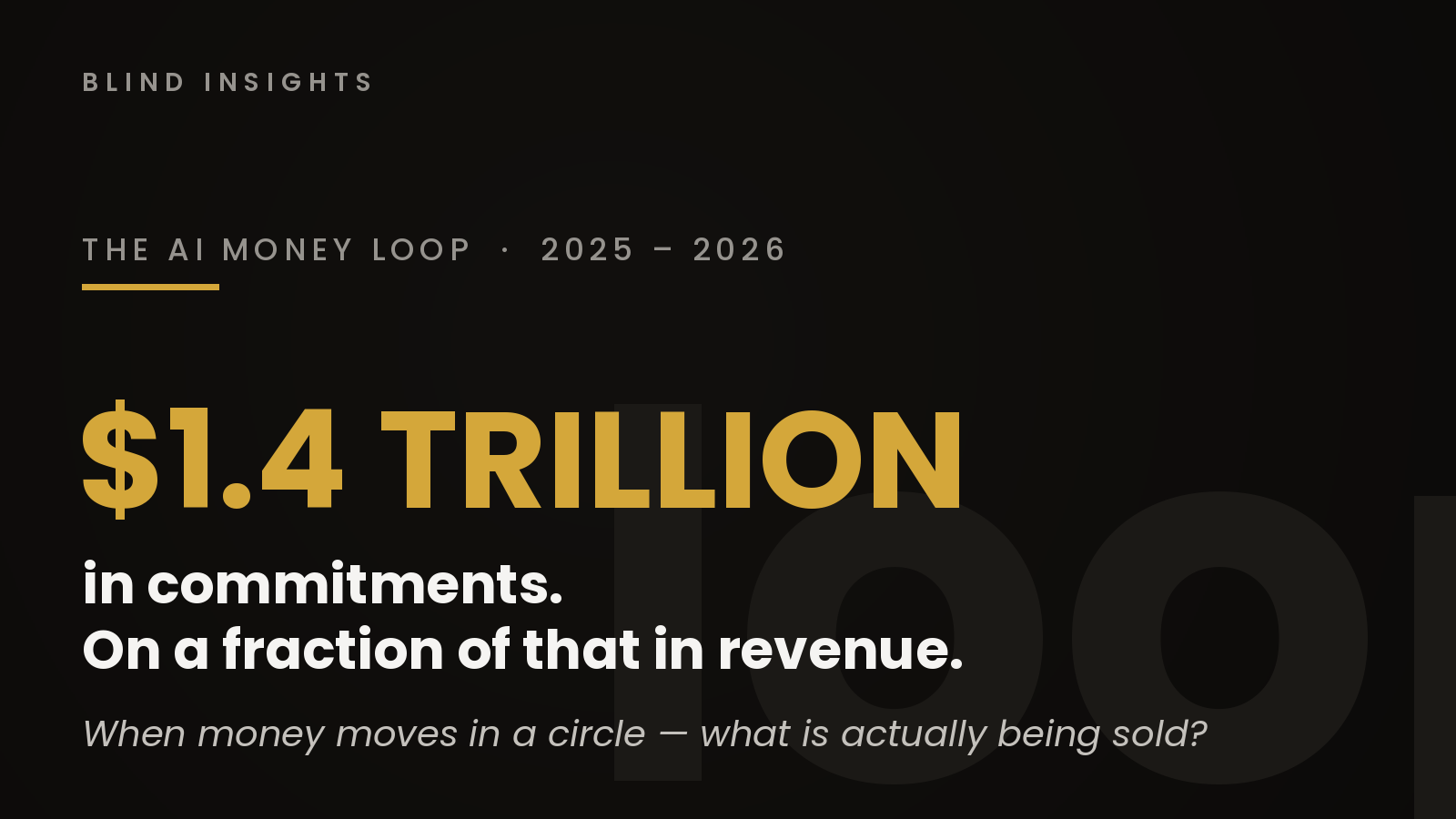

OpenAI’s revenue in 2025 was somewhere between thirteen and twenty billion dollars, depending on who is counting. Against that, the company has signed infrastructure commitments reported at roughly one and a half trillion dollars over eight years. Its projected operating loss for the single year 2028 has been put at seventy-four billion. One major bank estimated cumulative losses between 2024 and 2029 at around one hundred and forty billion dollars.

None of these numbers is secret, and none is necessarily fatal. Amazon lost money for years before it didn’t. But the gap between revenue measured in billions and commitments measured in trillions is precisely why the circular structure draws scrutiny. When the demand is uncertain and the financing is internal, the loop does most of the work of making the boom look inevitable — long before the end users have confirmed that it is.

The echo nobody likes to hear

We have watched a version of this film before.

In the late 1990s, telecom-equipment makers lent money to the new carriers so those carriers could buy their equipment. The loans were spent on gear. The gear was booked as sales. The sales validated the share price. The share price funded more lending. It worked beautifully — right up until everyone noticed there were not enough paying customers at the far end of all that fibre. Then the loop ran in reverse, and the reversal was faster than the build-up.

One prominent analyst group has called today’s arrangements reminiscent of the circular financing of the internet bubble. The comparison is fair as far as it goes. But there is a genuine difference, and intellectual honesty requires naming it: in the 1990s the financing was mostly debt. Today, a large share of it is equity — companies taking ownership stakes in each other at a scale that is, in fact, new. Whether that makes the structure more stable or more fragile is exactly the open question.

What this is not

This is not a prediction of collapse. It is not a claim that the AI build-out is fake, or that the demand will not arrive, or that anyone should sell anything. Plenty of serious people argue the demand is real and rising for reasons entirely outside the circle — and they may well be right.

The purpose here is narrower and, we would argue, more useful: to hand you the one distinction that lets you read every future headline about this boom for yourself.

The questions worth keeping

So the next time a record investment, a record backlog, or a record commitment crosses your screen, do not ask whether the number is big. It will be. Ask instead:

Is this dollar being counted once — or three times? Who is the end user, outside the circle, paying real money for the output? And what happens to every figure in the loop if a single node simply slows down?

We are not here to tell you how this ends. Nobody honestly can. We are here to make sure that when it does, you understood the mechanism before the headline did.

Blind Insights — clarity on money, the economy, and power. We look beneath the surface, because that is usually where the answer is. More at blindinsights.de.